TA QUANT WEEKLY MARKET INSIGHTS

MARKET SNAPSHOT

| Asset | Price | Weekly Change | Sentiment |

|---|---|---|---|

| BTC | ~$78,400 | +3.4% (wk) | Fear (recovering) |

| ETH | ~$2,310 | +0.9% (wk) | Fear |

| SOL | ~$84 | Flat | Neutral |

| Gold (XAU) | ~$4,620 | -3.2% (wk) | Under Pressure |

| Brent Crude | ~$108-111/bbl | +7.5% (wk) | War Premium Elevated |

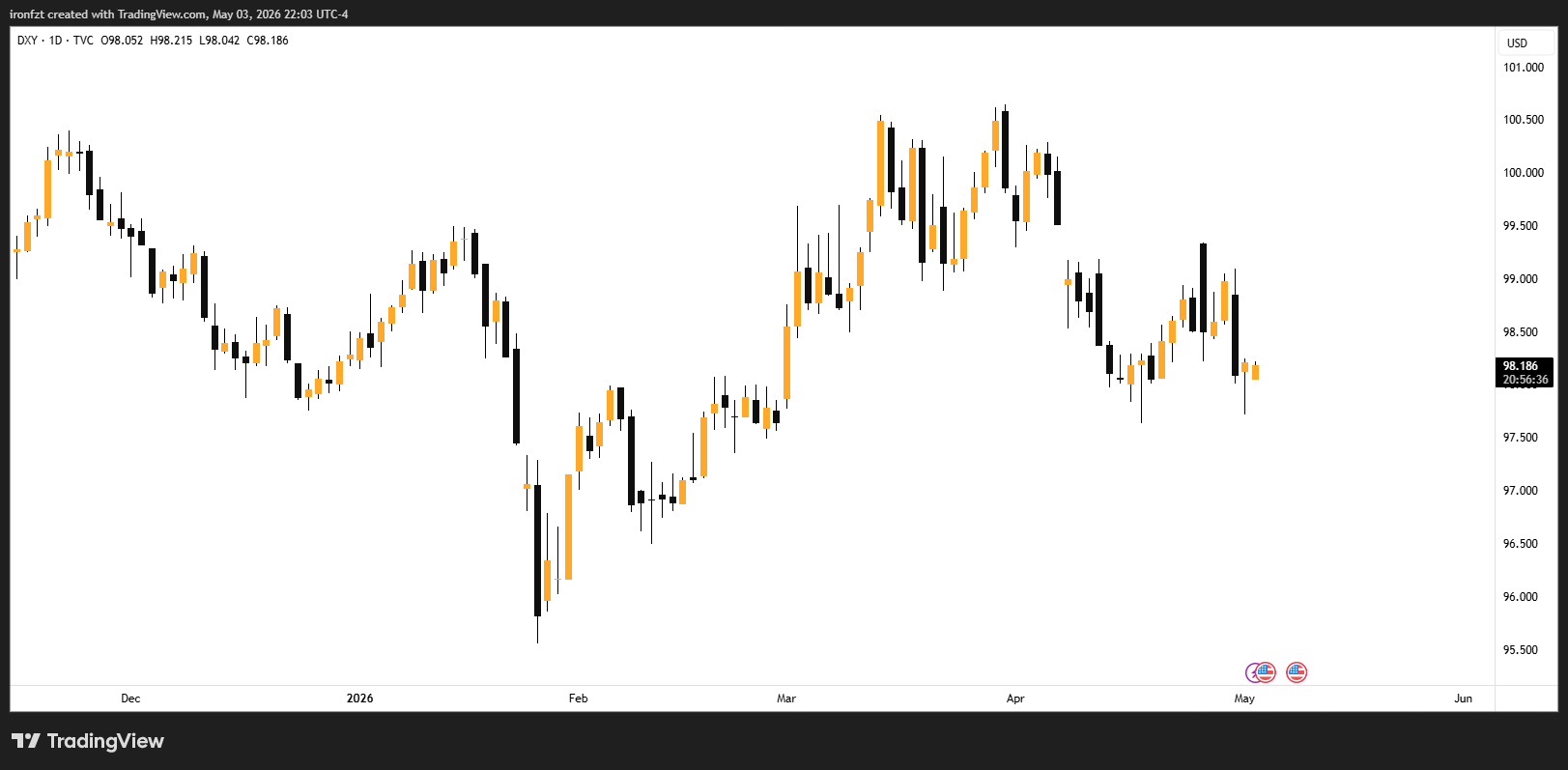

| DXY | ~98-99 | Two-month low | Weakening |

MACRO + GEOPOLITICAL: PROJECT FREEDOM AND A STALLED DEAL

The War Enters Month Three: Where Things Stand

The US-Iran war crossed the two-month ceasefire mark this weekend with no formal peace agreement in place and both sides signaling they are prepared to hold their positions indefinitely. The ceasefire, technically extended by Trump on April 21, remains in a gray zone. The US is actively maintaining a naval blockade of Iranian ports, while Iran continues to restrict commercial transit through the Strait of Hormuz. Both actions have been labeled violations by the opposing side.

The most dramatic development going into the week is 'Project Freedom,' announced by President Trump on Sunday May 3. Starting Monday, the US will begin escorting foreign vessels stranded in the Strait of Hormuz using a force that includes guided-missile destroyers, more than 100 aircraft, and approximately 15,000 service members. US Central Command was careful to clarify this is not a traditional escort mission, but Iran's response was immediate. Senior parliamentary official Ebrahim Azizi warned that any American interference in the strait constitutes a ceasefire violation and that the waterway 'will not be managed by Trump's delusional posts.' A vessel was also struck by unknown projectiles in the strait over the weekend, with all crew reported safe.

Project Freedom context: Around 20,000 seafarers remain stranded in and around the Strait of Hormuz after more than two months of blockade. One tanker captain told CNN: 'Ceasefire is not for seafarers. Ceasefire is for normal people.' The humanitarian dimension of the Hormuz crisis is now becoming a diplomatic pressure point.

On the diplomatic side, the week ended with a whimper. Trump canceled plans to send envoy Steve Witkoff and Jared Kushner to Islamabad on Saturday, writing on Truth Social that there was 'tremendous infighting and confusion within their leadership' and that Iran should 'just call' if they want to talk. Iranian Foreign Minister Araghchi had traveled to Islamabad over the weekend but met only with Pakistani officials before departing, signaling that direct talks remain deadlocked.

Iran did submit a fresh proposal. Pakistan confirmed Tehran sent an updated plan calling for ending the war on all fronts including Lebanon, with a push to resolve issues within 30 days rather than accept a two-month ceasefire extension proposed by Washington. Iran also separately floated reopening the Strait of Hormuz while deferring nuclear talks. Trump reviewed the proposal over the weekend and said he 'can't imagine that it would be acceptable.' A senior Iranian military official said renewed conflict is 'possible,' while Iranian media has reported that Tehran is preparing military relocations and 'new surprises' should the war resume.

The 60-Day War Powers Clock

A significant legal and political dimension has entered the picture this week. Under the 1973 War Powers Resolution, the president must notify Congress within 48 hours of committing US armed forces to hostilities, and those forces must be withdrawn within 60 days unless Congress authorizes the deployment. The 60-day clock is either approaching or has already passed depending on when you count from February 28.

Trump wrote to congressional leaders on Friday asserting that 'hostilities' with Iran have 'terminated' because there has been no exchange of direct fire since April 7. This framing is aimed at resetting or pausing the clock. Several Republicans have nonetheless signaled they want either a wind-down of operations at the 60-day mark or formal Congressional authorization. The legal ambiguity around whether a ceasefire with an active blockade constitutes 'terminated hostilities' is likely to generate significant political noise this week.

Fed Holds, PCE Spikes, and Warsh Waits

The Federal Reserve met in late April and held rates unchanged at 3.50-3.75%, but the decision came with four dissents, marking the most internal disagreement at the Fed since the early 2022 rate hike cycle. The division reflects a genuine split between officials who think energy-driven inflation is transitory and those who are increasingly worried about second-round effects.

PCE data released for March confirmed the inflation picture is deteriorating. The headline PCE price index rose 0.7% month-on-month, accelerating the annual rate from 2.8% to 3.5%. Core PCE also climbed to 3.2% annually. This is materially above the Fed's 2% target and reinforces the case for a hold. Markets are now beginning to price in the possibility of a rate hike in 2027, a scenario that was near-zero probability six weeks ago.

Kevin Warsh's confirmation to replace Powell, whose term expires May 15, is pending Senate committee vote. Markets assume confirmation given Republican Senate control. Warsh will inherit a policy environment where the inflation trend is moving in the wrong direction and the primary driver is a geopolitical conflict with no clear resolution timeline.

CRYPTO: BTC + ETH

Bitcoin: Through $78k, Targeting $80k

BTC closed April as its best ETF inflow month of 2026, pulling in roughly $2.44 billion in spot ETF net inflows, the strongest since October 2025. Price has responded accordingly, with BTC pushing through $78,000 to open May. CoinDesk flagged $78,557 as the price going into the week, up nearly 3% over seven days from last week's $76k close.

The technicals are increasingly constructive. BTC is trading above its 100-day EMA at $75,623, which has flipped to support. The RSI approaching 60 is elevated but not overbought. The ascending triangle that analysts identified last week remains intact, and a clean break above $80,000 is being widely watched as the trigger for a potential run toward $88,000-$93,300 (the 50% Fibonacci retracement of the macro move down).

One structural signal stands out. Bitcoin whale wallets holding more than 1,000 BTC have grown by 142 addresses over the past six months. Exchange reserves are at a 7-year low. Strategy (formerly MicroStrategy) continues to accumulate, now holding approximately 780,897 BTC representing nearly 3.8% of all circulating supply. These supply-side dynamics are compressing the available float at a time when ETF demand is firmly positive.

The one cautionary note is the futures funding rate anomaly. BTC's 30-day average funding rate has drifted to approximately -5%, against a historical norm of +8%. The standard interpretation is that institutional investors long on spot BTC via ETFs are simultaneously shorting futures as a carry or hedge trade. Historically, extreme negative funding periods resolve through short squeezes. BTC long/short ratio currently sits at 47.5% longs vs 52.5% shorts, a rare slight short majority that creates asymmetric upside if a squeeze develops into the $80,000 level.

Ethereum

ETH is trading around $2,310, essentially flat on the week after last week's institutional inflow momentum cooled. The $2,400 level has now been established as a clear multi-month ceiling, with multiple rejection wicks visible on the daily chart. A clean close above $2,400 would shift the technical focus toward $2,800.

On the regulatory front, a meaningful development came through the US Senate. The Clarity Act, which governs crypto market structure, cleared a key stablecoin yield hurdle. The final text blocks crypto firms from offering stablecoin yield products that structurally resemble bank deposits, but permits 'bona fide' staking and reward transactions. This removes a key legislative roadblock and represents meaningful progress toward a regulatory framework that institutional capital has been waiting on before increasing allocations to ETH-native DeFi.

The Tether Q1 report also provided a positive macro signal for the stablecoin infrastructure underpinning crypto markets. Tether posted $1.04 billion in Q1 profit and reported $8.23 billion in reserve buffers, reinforcing the health of the stablecoin layer that supports trading volumes across the ecosystem.

Altcoins and Broader Market

BTC dominance climbed to 60% as April closed, its highest reading in months. Stablecoin volume at $167 billion represents 137% of total 24-hour crypto market volume, confirming capital is queuing in stable assets rather than rotating into altcoins. This is not a classic altseason setup. Capital is defensive and majors-anchored.

The Consensus 2026 conference is opening in Miami this week, which historically injects a short-term narrative and price catalyst into specific sectors. Worth watching: the FOMC hold and the PCE data have actually slightly increased rate cut probability from near-zero to approximately 15% for late 2026, which is a marginal positive for risk assets. RWA tokenization has hit $19.32 billion in total value, up 256% in 15 months, and Hyperliquid controls roughly 70% of on-chain perps. These structural growth trends are attracting institutional attention even in the current macro fog.

GOLD (XAU/USD)

Gold is under significant pressure this week, trading around $4,620 after a rough end to April. The metal is now down approximately 15% from its pre-war peak, a counterintuitive move for a traditional safe-haven but one that reflects the specific mechanics of this crisis. Brent crude above $110 is pushing inflation expectations higher, which reduces rate cut probability, which in turn reduces the attractiveness of non-yielding gold.

The World Gold Council's Q1 2026 report, released last week, showed record global gold demand in the period. Total demand rose 2% year-on-year to 1,230.9 tonnes, with bar and coin demand up 42% to 474 tonnes, the second-highest quarterly figure on record. Asian investors were the primary buyers. The divergence between record physical demand and declining price reflects the overriding pressure from inflation expectations and the opportunity cost of holding a non-yielding asset in a rising-rate environment.

The DXY weakening to a two-month low around 98-99 is one of the few near-term positives for gold. Dollar weakness typically provides a tailwind for gold, which is priced in USD. The yen rally following suspected Bank of Japan intervention also contributed to dollar softness late last week. If DXY continues to slide toward the 95-96 zone, gold could see meaningful support, particularly if Iran talks show any sign of progress that would cap oil prices and ease the inflation narrative.

OUTLOOK: THE WEEK AHEAD

Project Freedom and the Hormuz Test

The single biggest market driver this week is the execution and reaction to Project Freedom. The US has committed significant naval assets to escort stranded vessels out of the Strait of Hormuz beginning Monday. If the operation proceeds without direct Iranian military response, oil prices could ease and risk assets including BTC would benefit. If Iran executes on its warning and treats the escorts as a ceasefire violation, the risk of renewed strikes is very real, and oil would spike above $115-$120.

Markets are watching Trump's framing carefully. He has told Congress that hostilities have 'terminated,' which would allow him to sidestep the War Powers deadline. But Project Freedom is an active military operation in a contested waterway against the explicit wishes of a country the US is technically in a ceasefire with. The legal and geopolitical interpretation of that is highly contested. Any resumption of direct fire would immediately collapse the ceasefire framework.

Key Events Calendar: May 4-8

- May 4: Project Freedom begins - US naval escort operation launches in Strait of Hormuz. Watch for Iranian response and any tanker incidents.

- May 5: Services PMI for April + JOLTS job openings data for March - Key read on service-sector inflation persistence

- May 6: ADP Nonfarm Employment Change for April - private payrolls preview

- May 7: Initial Jobless Claims - continuing signal on labor market health under energy inflation

- May 7-8: Consensus 2026 conference in Miami - industry catalysts, policy panels, potential narrative movers for specific sectors

- May 8: Nonfarm Payrolls (April) + Unemployment Rate + UMich inflation expectations. The most important macro print of the week.

- May 15: Jerome Powell's term as Fed Chair expires. Warsh confirmation vote expected beforehand.

TA Quant Positioning View

The dominant setup is a genuine binary. Project Freedom resolving without incident would be the first concrete positive development in this conflict since the original ceasefire, and it would immediately shift oil, rate, and crypto narratives. BTC is technically positioned to take out $80,000 on any meaningful geopolitical relief. The ETF bid is real, the supply float is compressed, and the funding rate anomaly creates a coiled short-squeeze setup.

The downside risk is symmetrically severe. Iran has stated clearly that it considers the escort operation a ceasefire violation. A single incident in the strait could restart the war. In that scenario, oil at $120+ would reprice every inflation-sensitive asset and put BTC back below $75,000 quickly. For market-making and algo strategies, this is a vol-expansion environment. Spreads are wide, catalysts are headline-driven, and the reward for getting the direction right before the market moves is substantial. Manage size, stay reactive, watch CENTCOM for any tanker incident reports.